2022-01-11 11:11

Reuters Institute-Oxford

To download PdF,for the Statistical Data Click Here

Executive summary | 1. The business of journalism is looking up for some | 2. Audience strategies and publisher innovation | 3. The practice of journalism: hybrid newsrooms, generational change, and new agendas | 4. Government regulation, privacy, and the future of platforms | 5. What's next | 6. Conclusions | Survey methodology | Acknowledgements | About the Author | Download a PDF version

2022 will be a year of careful consolidation for a news industry that has been both disrupted and galvanised by the drawn-out COVID-19 crisis. Both journalists and audiences have, to some degree, been ‘burnt out’ by the relentless intensity of the news agenda, alongside increasingly polarised debates about politics, identity, and culture. This could be the year when journalism takes a breath, focuses on the basics, and comes back stronger.

In many parts of the world, audiences for news media have been falling throughout 2021 – not an ideal situation at a time when accurate and reliable information has been so critical to people’s health and security. A key challenge for the news media this year is to re-engage those who have turned away from news – as well as to build deeper relationships with more regular news consumers.

Generational change will also continue to be a key theme, leading to more internal soul-searching in newsrooms over diversity and inclusion, about emerging agendas such as climate change and mental health, and about how journalists should behave in social media.

On the business side, many traditional news organisations remain relentlessly focused on faster digital transformation as rising newsprint and energy costs look to make print unsustainable in some countries. Charging for online news is the end-destination for many, but expect subscription fatigue to limit progress, especially if economic conditions worsen.

After a period where digital advertising revenue has leaked away to giant platforms, publishers have an opportunity to secure better results this year. Tighter privacy rules limiting third-party data, along with concerns about misinformation, have already started to swing the tide back towards trusted brands, but advertising remains a competitive and challenging business, and not every publisher will thrive.

Meanwhile the talk of platform regulation becomes real this year as the EU and some national governments try to exercise more control over big tech. However, next generation technologies like artificial intelligence (AI), cryptocurrencies, and the metaverse (virtual or semi-virtual worlds) are already creating a new set of challenges for societies as well as new opportunities to connect, inform, and entertain.

How do Media Leaders View the Year Ahead?

Other Possible Developments in 2022

One of the biggest surprises in this year’s survey is the growth in revenue reported by many publishers. Well over half our sample (59%), which includes both subscription and advertising focused publishers from more than 50 countries, say that overall revenues have increased, with only 8% reporting that things had got worse. This is despite the continuing COVID-19 pandemic and the further erosion of traditional revenue sources such as print.

In many ways this is testament to the adaptability of an industry that has accelerated new digital revenue streams such as subscription, e-commerce, and digital events over the past 18 months – and also started to bring in substantial licensing revenue from tech platforms on top. For all publishers, a key element in this has been a strong bounce back in digital advertising, as consumers moved their spending online during the ongoing pandemic. Digital advertising grew at its fastest rate ever (30% year on year) in 2021 according to GroupM and now accounts for around two-thirds (64%) of all advertising spend.1

It is worth remembering that many publishers not represented in our survey still rely on traditional and declining revenue sources such as print and even broadcast. And for those without a clear digital path ahead of them, the outlook remains extremely challenging.

At the same time, overall consumption of online news has fallen significantly in some countries, including the UK and the United States, following the dramas of the Trump era, according to industry data. The relentless and depressing nature of the news has been a factor, with many consumers looking to social media and streaming services for entertainment and distraction.

In our own survey, covering a wide range of countries, we find a more mixed picture. Although the majority (54%) report static or declining traffic to online news sites, more than four in ten (44%) say their traffic has gone up.

Overall, the majority of publishers (73%) say are optimistic about the year ahead. Even if traffic is down in some cases, journalists feel that their role is more valued by audiences and the business side in particular is on a more solid footing.

Journalism is no longer being taken for granted. The industry is explaining itself better and money is flowing proportionately to economic growth.

David Walmsley, Editor-in-Chief, Globe and Mail, Canada

Levels of confidence in journalism more generally (60%) are a bit lower, especially in countries where there is political polarisation, economic weakness, and where journalists themselves are under attack:

The power of governments against free press or journalism is growing in Latin America (especially Mexico). The president can say whatever, even if he is openly lying, press debunking or explaining the lie has little effect [by comparison].

Senior journalist, Mexico

We’ll come back to the pressures on journalists later in this report.

A key part of publisher confidence has been the continued growth of subscription and membership models through the COVID-19 pandemic. The New York Times now has 8.4 million subscriptions, of which 7.6 million are digital, putting it on track to hit its 10 million target by 2025.2 For many of these early-movers, digital revenue now outstrips print and many upmarket titles can see a path to a sustainable future. But so too can a number of smaller digital-born publishers with significant reader revenues, such as Dennik N in Slovakia, El Diario in Spain, Malaysiakini in Malaysia, Zetland in Denmark, and the Daily Maverick in South Africa.

The opportunity for growth at the company level is there for us. We see the path and prospects clearly now with sustainable revenue model in place.

Styli Charalambous, CEO, Daily Maverick, South Africa

Subscription remains the number one priority (79%) for commercial publishers in 2022, according to our survey, ahead of display advertising (73%) and native advertising (59%), events (40%) and funding from platforms (29%), which has grown significantly over the last year.

The jury is still out on whether subscription models will work for all. Alternatives are being pursued by publications such as BuzzFeed and Vox, working across a range of brands to give them more scale. These brands still see a future with a mix of models – from advertising, to e-commerce, and even reader payment too. Once again, our survey shows there is no one-size-fits-all model. Advertising continues to be the main focus for many, and commercial publishers cite, on average, three or four different revenue streams as being important or very important to them this year.

Free at the point of consumption models will also be important in ensuring that news is not just for elites. Almost half of news leaders (47%) worry that subscription models may be pushing journalism towards super-serving richer and more educated audiences and leaving others behind. Many leaders of PSBs and others committed to open journalism are amongst those who disagree with this statement, but our own research shows that even these organisations are struggling to build connections with younger and less educated groups online.3

What will happen this year?

Open access initiatives: Expect more deals for those from disadvantaged backgrounds as a way of countering critiques about growing information inequality. The Daily Maverick in South Africa offers a ‘pay what you can afford’ membership and El Diario in Spain allows people to pay nothing at all. In Portugal, lottery funding has been used to fund 20,000 free digital news subscriptions for eight media outlets. The weekly magazine Visão gave some of these funded free subscriptions to older people attending the University of the 3rd Age while Público targeted unemployed people as part of its allocation, and Correio da Manhã decided to help older people living in care homes. Others, like Politiken in Denmark, are looking to extend schemes offering free access for students to educational institutions.

Making subscriptions more accessible

Countering subscription fatigue via product extensions and bundling: This will be a key focus for many publishers looking to hang on to new subscribers gained during COVID. Cut-price offers and differential pricing will be one likely response, especially if the economy cuts up rough, but others are looking to develop new premium products to encourage tie-in. The New York Times has led the field with the success of its crosswords and cooking apps. Now it has moved its product review site, Wirecutter, behind a paywall and has also started offering previously free newsletters from star writers like Kara Swisher only to subscribers.4 Other publishers are looking to bundle paid podcasts and audio books.

Over the last few years, we have seen the coming together of two powerful ideas. The first is that online journalism needs to be paid for and the second that journalists may need to behave more like social influencers as they build relationships and communities.

These ideas are embodied in new platforms like Substack, which along with new product offerings from giant tech companies have enabled individual writers, vloggers, and podcasters to make significant amounts of money, injecting new life into the so-called ‘creator economy’. In November Substack announced that it had hit the milestone of 1 million paid subscriptions, with top writers earning six-figure sums from its newsletter focused platform.5 Both Facebook (Bulletin) and Twitter (Revue) have launched their own competitors to Substack, along with a range of other features to incentivise creators. Twitter, for example, in September 2021 launched a Super Follows subscription feature (think bonus tweets) that helps creators earn money from their most engaged fans.6 Facebook introduced fan subscriptions and stars, both mechanisms that provide financial rewards for the most engaging content. Meanwhile podcast platforms are enabling similar features with a subscription or donation offer on top of a free service. These developments are setting up new dynamics around who gets attention and what content may be prioritised in years to come.

What will happen this year?

Mainstream media poaches back: If last year’s trend was star writers setting up on their own, this year we may see more movement in the opposite direction. Not all writers have found it easy to grow an audience quickly on their own and traditional companies are looking to hoover up talent as a way of feeding subscription pipelines. The Atlantic, for example, is launching a suite of new newsletters including writers like Charlie Warzel, who previously operated his Galaxy Brain brand on Substack. Writers can continue to earn money independently from podcasts and personal appearances and existing followers get a year’s free access to The Atlantic, after which they will need to subscribe.

Journalism collectives as a halfway house: This year we may see more companies that try to mix the infrastructure of a traditional news organisations with the freedom and financial rewards they can find on their own.

Puck is a start-up founded by a former editor of Vanity Fair Jon Kelly, who has brought together a set of writers to cover Silicon Valley, Hollywood, Washington, and Wall Street. ‘There is an elite group of journalists who want to have a direct connection with the large audiences they’ve amassed on social channels’, says Kelly.7 Founding partners own part of the business but also get bonuses based on the subscriptions and ad sales they generate. For an annual fee, consumers get access to emails across a range of subjects but can also pay a premium for events and personal access to writers.

Connecting writers pay to subscriptions: This is likely to become an increasingly contentious issue this year as media companies rely more on star talent to generate revenue from readers. Puck has an algorithm that works out how to reward those driving most revenue but transparency and fairness will be tested. Casey Newton, one of the current Substack stars, thinks that publishers will eventually need to offer shared revenue on newsletters or video sponsorships or podcast ads: ‘I expect lots of thrashing from journalists who think they have the right to experiment with Super Follows and other creator monetisation tools and publishers who want to shut them down.’8

All this activity is creating more and more content, but the big question is whether there are enough people with sufficient interest to pay for all but the star writers and podcasters.

It wasn’t that long ago that BuzzFeed and a few other digital native brands, such as Vox and Vice, looked like the future of the news business. Sky-high valuations were fuelled by a generation of writers comfortable with digital culture, who invented a set of formats that matched rising consumer enthusiasm for social consumption.

But this open access, ad-supported model has taken a knock following various Facebook algorithm changes, compounded by the shock of coronavirus. Some of the stars of digital media have defected back to old media companies and many venture capitalists (VCs) are looking to get their money back. The original disrupters are now caught in a battle with resurgent legacy media for general readers and with platforms for advertising dollars.

What will happen this year?

Digital natives go for scale: BuzzFeed founder Jonah Peretti has argued for years that digital publishers should consolidate to give them more leverage with advertisers and compete with the ad dominance of Facebook and Google. BuzzFeed’s move to go public, completed in December 2021, provided the cash to acquire digital lifestyle publisher Complex, following last year’s purchase of HuffPost.9 Now all eyes will be on Vice, Vox, and Bustle as they contemplate similar moves. Vox bought New York Magazine and its websites in 2019 and has just acquired Group Nine (owner of multiple brands including NowThis and PopSugar). By year end we can expect more M&A activity but perhaps not the mega-merger that was predicted some years ago.

Traditional media look to acquisition to fuel growth: The biggest players will be looking for digital brands that can add value to their subscription bundles and bring different types of audience. Axel Springer purchased Politico last year for around $1bn and the New York Times has agreed to buy subscription-based sports site The Athletic, in a deal valued at around $550 million. The Athletic has built built more than 1 million subscribers based on deep reporting in multiple sporting niches.10

Local start-ups fuelled by new models: At a local level, we can expect to see the growth of low-cost reader-focused start-ups this year, built on newsletter platforms like Substack, which help take out technology and infrastructure costs.

The Manchester Mill, which launched during the height of COVID lockdowns, has generated almost 1,000 paying subscriptions at £7 a month in the last year for a mix of slow journalism delivered mainly by newsletter. A certain amount of free content gives it a much wider readership and there is now an offshoot in print.11 Super users engage with the editorial team on a Facebook group providing ideas for stories. And there is a podcast too.

A sister title, the Sheffield Tribune has gained around 300 subscribers and a third, The Post, has just launched covering Liverpool.

Meanwhile in the United States, Axios has plans to expand its newsletter-led model to 25 cities by mid 2022 – with 100 soon after. Axios reporters will break local news, hold local officials accountable and offer tips for navigating local areas and hopes that this reader-supported (membership) model can eventually reach ‘every community in America’.

Following the shock of COVID, the key mood in our survey this year seems to be around consolidation when it comes to product development. Although some media companies are focusing on advertising and others on subscription, the success of both models ultimately depends on deeper engagement with audiences via websites, apps, newsletters, and podcasts.

In terms of audience-facing innovation, most effort this year will go into podcasts and other digital audio (80%), followed by building and revamping newsletters (70%) and developing digital video formats (63%). By contrast, ‘shiny new things’, involving technology that has not yet reached maturity, such as applications for voice (14%) and the metaverse (8%) appear to be largely on the backburner.

Growing consumption of digital audio has been a trend for a few years, driven by a combination of smartphones, better headphones, and investment in podcasts from platforms like Spotify, Google, and Amazon. But in the last year we’ve seen the rapid development of a much wider range of digital formats such as audio articles, flash briefings, and audio messages, along with live formats such as social audio.

The rise (and fall) of Clubhouse, known as the first ‘airpods social network’, has been well documented but almost all the major platforms, such as Twitter (Spaces), Facebook (Live Audio Rooms), Reddit (Talk), quickly produced clones to allow users to create impromptu discussion and events. The jury remains out on how compelling audiences will find these features when the hype dies down.

More widely, the platforms are investing in tools to allow consumers to create and edit their own short audio stories – effectively delivering another layer of the creator economy. Facebook/Meta are building ‘soundbites’, a new creative, short-form audio format that will appear across all their products – a sort of TikTok for audio.

Audio is going to be a first-class medium. Every once in a while, a new medium comes along that can be adopted into a lot of different areas.

Mark Zuckerberg, CEO Facebook12

Meanwhile audio messaging and communication is gaining traction and finding a new home in a range of apps from cooking to dating. Short audio messages attached to dating profiles within Hinge have added a sense of personality beyond photos and bios – and many have gone viral.13

Implications for journalism

Platform investments in audio are opening up the medium to anyone with a smartphone and a story to tell, but this is likely to create a set of familiar problems for publishers. More content means more competition for attention and it may be harder for professional content to stand out. On the other hand, it may also stimulate listening overall, enabling more opportunities for consumption and connection. For platforms, there will be new content moderation challenges in a medium even harder to monitor than written text.

In our conversations around trends and predictions, it is clear that many publishers believe that audio offers better opportunities for both engagement and monetisation than they can get through similar investments in text or video. At least in the United States, podcast CPMs have been buoyant through the pandemic with the New York Times making $36m from podcast ads according to their 2020 results.14 Equally important though is the value in marketing and attracting new audiences. Tortoise Media, which has pivoted heavily towards audio, ended the year with the No. 1 podcast on the Apple Podcast charts in the United States, Sweet Bobby, introducing many more people to the brand, including much-sought-after younger listeners.

What will happen this year in audio?

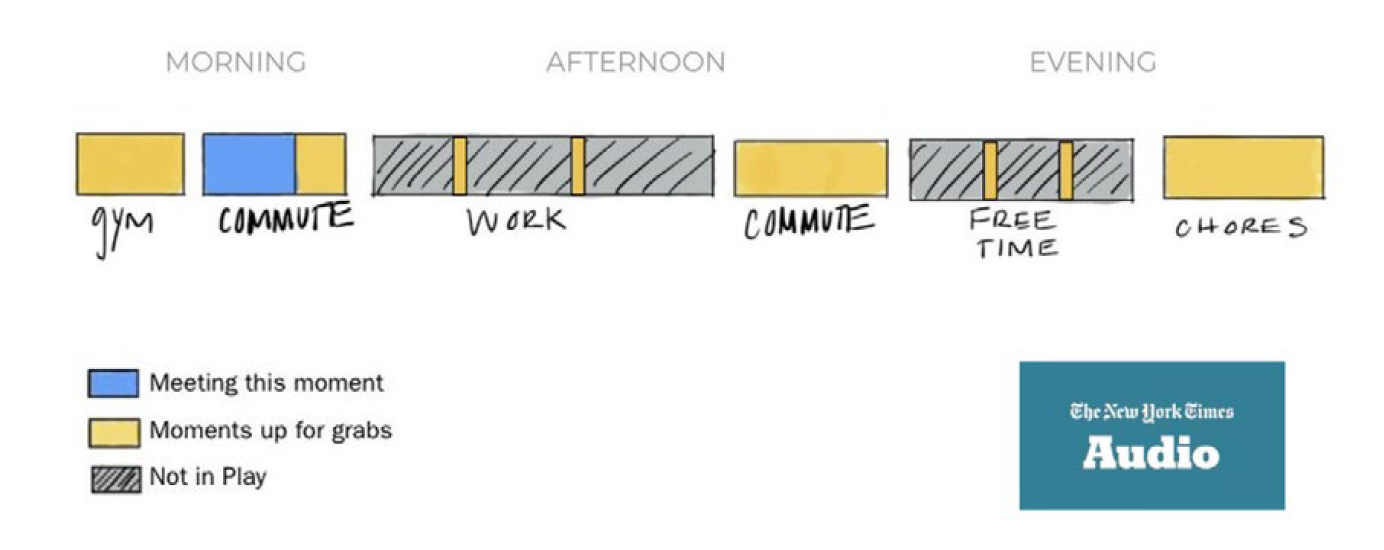

More publishers look to become audio destinations of their own: With audio becoming more central, the battle is on between competing platforms and publishers to control the full customer experience. The New York Times is planning to launch a listening product this year which will include article narrations from Audm including stories from rival publications, and shows from Serial Productions, both of which it bought in 2020. It is also likely to include the 25-year archive from public radio programme This American Life. It is also possible that it will feature a long-expected afternoon version of The Daily, the hit podcast that has more than 20 million listeners monthly. In developing the app, the Times has spent identified key ‘moments’ where consumers may be open to audio-only experiences – and its analysis shows that the current offer (in blue) is only scratching the surface.

The new app may end up part of the Times subscription bundle, or at least in a premium layer within it. This is another key reason why audio is seen as strategically important. It can deliver reach, loyalty, and revenue in equal measure. Schibsted is also building free and premium audio products in Nordic countries, following the acquisition of Swedish platform PodMe, and says that audio, which includes podcasts, books, and short-form content, is now a core part of its overall strategy.

Elsewhere, some public broadcasters have been considering whether to host podcast content from other publishers and are withholding their best content from the big tech platforms for a period of time.

Second coming for paid podcast platforms: Paid features from Apple and Spotify will open up the market this year for individual creators and publishers alike this year. Unlike Apple, Spotify is not taking a cut for the first two years in a bid to encourage the best talent. Options include offering a mix of free and paid content, including bonus episodes for super fans. Independent podcast platforms are also quietly creating alternatives, especially in smaller markets. Podimo has 100,000+ paying subscribers for high-quality local language content in countries like Denmark, Norway, Germany, and Spain, and has secured funding for further expansion of a model where it shares membership fees with those creating the content. But with publishers joining platforms looking for the best exclusive content expect the price to go up this year, especially for the biggest stars.

The first pivot to video was partly driven by new social media formats like Facebook Live, but quickly faded after the platforms lost interest. Now live video is booming again, partly fuelled by COVID news conferences and dramatic events like the storming of the US Capitol, while short-form video has been revitalised by the creativity and dynamic growth of TikTok.

Publishers are stepping up investment, with NBC, as one example, adding 200 new positions and several new hours of programming for its NBC News NOW service which also feeds the Peacock streaming service.15 It has also invested heavily in short-form video reaching tens of millions of Gen-Z viewers with its Stay Tuned programming on Snapchat.

Meanwhile TikTok now reaches more than a billion people around the world, according to the company. Users have been captivated by its mix of music, humour (and news) driven by a powerful ‘For You’ feed generated by an algorithm that learns what you like. In turn this success has led Facebook and YouTube to step up development of their own copycat formats (Reels and Shorts), further fuelling creation and promotion of this content.

Our own Digital News Report found that TikTok now reaches a quarter (24%) of under-35s, with 7% using the platform for news – even more in parts of Asia and South America. But our research also found that, when it comes to news, it is mainly influencers and celebrities that people are paying attention to – raising questions about how and whether journalists and news brands should engage on this platform.16

Why does this matter for journalism?

Publishers are increasingly worried about how to attract younger audiences and many see native video formats as part of the answer. The Swedish Public Broadcaster SVT is now the number one destination for a quarter (26%) of Swedes aged between 20 and 29 years old – up from just 9% in 2017. Much of that change is due to investment in a range of mobile-friendly online video formats that get to the point quickly or address non-traditional subjects.17 Other public broadcasters like Germany’s ARD have been experimenting with creating more bespoke video content for third-party platforms like TikTok and Instagram.

In our survey, we can see a clear change in direction in terms of the third-party platforms being prioritised this year. Publishers say they will be putting much more effort into Instagram (net score of +54), TikTok (+44), and YouTube (+43), all networks that lead with visual and video content, and less effort into general purpose networks like Twitter (-5) and Facebook (-8).

What will happen this year in video?

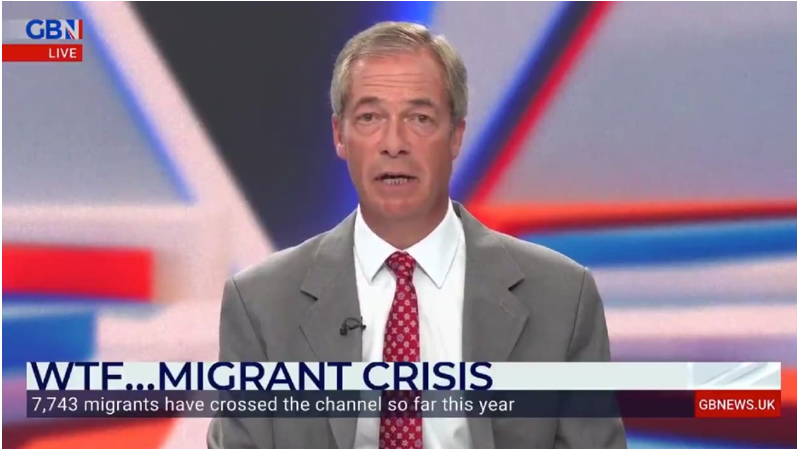

Influencers build mass audiences via networks like Twitch: Ibai Llanos, a Spanish influencer with 7 million followers on the gaming platform Twitch, secured the first interview with footballer Lionel Messi after his transfer to Paris Saint Germain, outcompeting traditional broadcast journalists. More than 300,000 people watched the original broadcast, with more accessing on demand. Llanos is an example of a new generation of entrepreneurial stars who are creating and monetising their communities across a number of platforms. Politicians are also looking to interact on a platform that is especially popular with e-sports fans and young men.

News on TikTok remains a battleground: Publishers looking to crack the code of TikTok’s bite-sized videos are being shown the way by a Spanish start-up. Ac2ality has built up around 3 million followers on TikTok for a service that includes a one-minute round-up of top stories. That’s more followers than the Washington Post and the BBC combined. With more news on TikTok, expect more false and misleading information too. The Institute for Strategic Dialogue recently tracked vaccine misinformation on the platform and found that just over 100 posts had got more than 20 million views thanks to TikTok’s powerful algorithm and unique audio features designed for virality.18 Some outside observers continue to worry that the Chinese-owned platform will take a different approach to content moderation on politically sensitive topics than its US-owned competitors.

One start-up looking to counter misinformation on TikTok and other social-platforms is the News Movement, founded by former executives from Dow Jones and the BBC. The service aims to deliver trustworthy and objective information in 2022 to mass audiences on social media, with accessible video explainers as well as text. The News Movement is staffed by young journalists and will operate across TikTok, Instagram, YouTube, Facebook and Twitter.

Social shopping takes off: Expect to find news mixed with more online shopping this year as Instagram, TikTok, and Snap lean into e-commerce. Whether it’s sportswear or make up, consumers are increasingly browsing, discovering, and buying items on social media platforms and the sector is expected to grow in the US alone from $36bn in annual sales to $50bn by 2023, according to research firm eMarketer.19 Some publishers are looking to cash in, with NBCUniversal experimenting with a show on Instagram, while TikTok has hosted a two-day live-streamed event in the UK with influencers, music, and a quiz. Meanwhile, Snap is investing in augmented reality technology to help users virtually try on items like watches and jewellery.

Social shopping takes off: Expect to find news mixed with more online shopping this year as Instagram, TikTok, and Snap lean into e-commerce. Whether it’s sportswear or make up, consumers are increasingly browsing, discovering, and buying items on social media platforms and the sector is expected to grow in the US alone from $36bn in annual sales to $50bn by 2023, according to research firm eMarketer.19 Some publishers are looking to cash in, with NBCUniversal experimenting with a show on Instagram, while TikTok has hosted a two-day live-streamed event in the UK with influencers, music, and a quiz. Meanwhile, Snap is investing in augmented reality technology to help users virtually try on items like watches and jewellery.

The big question is whether any of this will work for news publishers. Previous attempts to monetise short-form social video have proved unsuccessful, while e-commerce is most suited to lifestyle brands and breaking news is largely commoditised. Despite this, CNN has taken a brave decision to put its live stream behind a paywall as part of a CNN+ service that will include exclusive on-demand shows. Many other broadcasters will be looking carefully at how that works out in 2022.

Most survey respondents are clear that the main focus this year should be on iterating and improving existing products (67%), rather than investing in new technologies or services (32%). This is partly because publishers have less money available for risky investments but also because most publishers now have a clear path on which they are set. A good starting point is to ensure that existing digital products are as seamless and engaging as those produced by tech platforms. News products have often fallen far short.

In terms of specific initiatives, a number of publishers talked about the need to replace legacy apps, optimise subscription pipelines, and upgrade their data infrastructure. While most are focusing on the core, we also find a small minority of well-funded leading-edge publishers pushing hard for growth, strengthening their business models through brand extensions and acquisitions. The New York Times has found growth with cooking, crosswords, and shopping, and others are looking to adopt similar approaches.

Innovation is becoming a more important part in our growth strategy as we try to go beyond the ‘core’.

CTO at a successful subscription publisher

Innovation blockers in the year ahead

Publishers recognise that innovation is critical in making sure that they stay relevant as audience behaviours continue to shift. But our survey suggests that, although the strategy is often clear, delivering planned improvements can be a different issue.

Around half (51%) of our sample of publishers say that they don’t have enough money to invest in innovation this year, partly due to budget cuts imposed during COVID. A similar proportion say they are struggling to hire or keep enough technical, design, or data staff to deliver solutions. In our Changing Newsrooms report we found the biggest concerns about talent were around software engineers and data scientists.

Another major barrier to innovation highlighted by the survey includes lack of alignment (41%) between different departments such as editorial, marketing, commercial, and technology. We have previously highlighted how the vertically siloed nature of many media companies makes it particularly difficult to deliver innovation that needs cross-functional teams to work in a common process. ‘We’re now in an age of mature product departments’, says Chris Moran, Head of Editorial Innovation at the Guardian. ‘But we still need to work to find the right balance between the rigour of product methodologies and processes and the specific editorial expertise of a given publisher.’

Moran argues that, if organisations want to innovate the process, they should not start with shiny new technologies like VR or AI: ‘It’s about the right technology applied intelligently in ways that tie to our values and expertise. That way we will build genuinely unique features and products that differentiate us from platforms and their associated problems.’

Almost two years into the pandemic many newsrooms are unrecognisable, some remain largely empty. But journalists are also struggling to cope with burnout from a relentless news cycle which has often impacted their own health, attacks by politicians, harassment on social media, and the isolation that comes with working from home. Behind the scenes much has changed. A new generation of leaders is taking over with a new agenda and more inclusive approach.

Assuming that the virus is finally brought under control, this will be the year when hybrid working – with some people in the office and others working remotely – becomes the norm. Our Changing Newsrooms report in November found that news organisations are pressing ahead with plans to redesign offices, upgrade technology, reduce desk space/office space, and renegotiate contracts with employees to accommodate this shift. Over the next year we can expect most employees to spend two to three days a week in the office and the rest at home.

Yet our report also found that the full implications of the hybrid newsroom have not been fully worked through. The experience so far has been good for efficiency, but publishers worry about losses to creativity, collaboration, and communication (3Cs).

What can we expect this year?

More fully virtual news organisations: Expect to see more publishers closing offices entirely, or at least moving in that direction. Last summer, the business-focused publication Quartz announced it was becoming a ‘fully distributed company’. This means it will employ anyone from anywhere, opening up the talent pool and reducing costs. Though Quartz has kept the lease on its New York office for another year, the assumption is that, in terms of meetings, ‘even when you are at the office, everyone is remote’, says CEO Zach Seward.20

Source: QZ at work.

Meanwhile in the UK, regional publisher Reach has closed 75% of its offices, turning staff into remote workers, while another publisher, Archant, is closing two-thirds of its offices by March 2022, arguing that home working is now the preferred option for most employees.

This risks undermining company culture but may be more equitable than hybrid environments, where ‘proximity bias’ can favour those prepared to show their face in the office every day. Hybrid working will also require clearer rules, better training, and a new literacy for both managers and staff.

Rethinking offices as spaces for community events: With fewer staff in the office, some publishers have been looking to reuse space to engage audiences. Expect to see more attempts to mix the intimacy of a live event with engaging a larger crowd online. UK slow news start-up Tortoise Media, whose business model is underpinned by events, has worked hard to improve its hybrid events over the last year, using interactive elements to keep remote audiences engaged and increasing the sophistication of its production.

Greater focus on mental health: While home working has been a boon for many, others have found the experience extremely challenging. To help counter isolation, UK regional publisher Reach has organised online book and film clubs, and social cook-alongs. Staff also get a free subscription to a mindfulness app (Headspace), an online wellness hub, as well as access to psychological counselling if needed. Expect to see other publishers to adopt these approaches in 2022 and provide extra training for managers on how to support staff effectively.

It’s not only journalists who have been feeling the pressure. Our own research at the Reuters Institute consistently finds that audiences often feel overwhelmed by the amount of news, with many saying they regularly avoid the news because it is too depressing.21 These trends have been compounded by the relentlessly negative nature of the news over the last year about COVID-19 and climate change.

At the same time the pandemic has forced many newsrooms to reassess their editorial approach. Remote working is breaking down hierarchies and a new wave of editors are embracing a more positive and diverse agenda. In 2021, partly in response to the gender and racial reckonings of the last few years, a number of the most prized roles in US media were filled by female journalists, many of them women of colour.

Diversity progress shift reaches beyond United States: The lack of diversity and lack of equity in journalism are well documented and won’t be solved this year, but more publishers are now openly acknowledging the damage this has done in terms of public trust and audience attention. Announcing the appointment of Washington Post’s first female Executive Editor, Sally Buzbee, publisher Fred Ryan made clear they were looking for a leader who would ‘prioritise diversity and inclusion in our news coverage as well as our hiring and promotion’.22

A recent Reuters Institute factsheet23 highlights how progress is still unevenly distributed. Across 12 strategic markets, less than a quarter (22%) of top editors are women, but this ranges from 60% in South Africa to 0% in Japan. Despite this, our recent Changing Newsrooms survey found that most publishers feel they are doing a good job in addressing gender diversity but have more work to do elsewhere. Ethnic diversity remains the biggest priority (35%) for media companies this year in terms of improving newsroom diversity.24 Outside the US we can expect much more focus on recruitment of journalists from minority groups this year as well as the way they are portrayed in the media. Greater diversity may also become more of a business imperative this year, with younger readers in particular paying close attention to content that speaks to or serves their identity.

Constructive formats: A more diverse set of editors is also questioning traditional assumptions about how to cover the news. Many are looking for alternatives to confrontational talk shows and divisive columnists. Swedish TV national editors are now required to include one constructive item a day in their main nightly show and local teams have targets around in-depth coverage.25 Research suggests these solution-orientated formats appeal more to younger audiences and that people feel better informed and more empowered after watching or reading constructive stories.26 Meanwhile the Constructive Journalism Institute in Denmark has been pioneering formats such as ‘Solved or Squeezed’ in conjunction with a local TV station, where politicians from different political parties are challenged to come up with solutions to a specific problem as their physical space gets more restricted over a 20-minute period. Following positive feedback from politicians and audiences they plan to iterate and repeat the format this year.

Elsewhere a TV station has experimented with putting politicians in the audience to listen to the views of ordinary people and in similar vein the Guardian has introduced a format where people with different perspectives come together over a meal to find common ground.

Explanatory formats become viral hit: The increased complexity of stories such as COVID-19 has led to a renewed interest in explanatory, often data-rich, online formats. At the BBC, presenter Ros Atkins has been encouraged to further develop a style of no-nonsense analysis of complex events boiled down into five- to ten-minute monologues aimed at digital audiences. These are heavy on facts, beautifully produced, but delivered in a deadpan and impartial way. Recent videos about Boris Johnson’s Christmas party woes attracted 11 million views in just a few days – a far bigger audience than could have been achieved on TV alone.

But in 2022 these fact-based formats will face a further challenge from opinionated hot takes also eyeing social media attention. GB News suffered a disastrous launch and torrid first year, at various stages receiving official TV ratings of zero viewers, but often boasting about its impact on social media. Rupert Murdoch’s Talk TV is waiting in the wings and is likely to stretch impartiality rules to the limit in the UK. Meanwhile in the US, with mid-term elections due and a new social network from Donald Trump on the way, the battle of facts vs opinion will continue to play out this year in unpredictable ways.

The awarding of the Nobel Peace Prize to two fearless journalists, Maria Ressa from the Philippines and Dmitry Muratov from Russia, has highlighted the political and physical harassment faced by reporters around the world. Much of this is driven by political polarisation, but in some countries it has been further exacerbated by the way that social media have been weaponised. A recent report by the International Center for Journalists documented the extent of the harassment of Maria Ressa and her colleagues in the Philippines, while an accompanying survey of 900 women journalists found that nearly three-quarters had experienced online abuse.

Elsewhere anti-vax protesters have also turned their anger on journalists. In the Netherlands several journalists were physically attacked in a context of growing hostility towards the press. The Head of News at public broadcaster NOS, Marcel Gelauff, says his journalists are facing ‘polarisation in society, aggression, harassment, and ongoing accusations of fake news’. In the UK BBC reporter Nicholas Watt was hounded through the streets of London by a group of anti-lockdown protestors, with footage shown live on YouTube. In Los Angeles volatile protests over trans rights and opposition to masks and vaccines led to at least seven journalists being assaulted over the summer.

What can we expect this year?

Publishers step up support: This year we’ll see publishers providing more support for journalists, including security protection for TV crews and better training. The UK’s largest regional publisher, Reach, is appointing its first online safety editor to tackle ‘endemic abuse and harassment of its journalists head on’ and we can expect others to do the same. More widely, the EU says it will bring forward a media freedom act in 2022 to safeguard independence, after a number of recent murders of investigative journalists allied to concerns about the capture or suppression of independent media in member states like Hungary and Poland.

New rules for social media: Polarised debates in social media are also making publishers rethink the ways in which journalists should engage in networks like Facebook and Twitter. After concerns about reputational damage, many news organisations have been tightening their social media rules. The BBC’s new guidelines, for example, include a ban on ‘virtue signalling’, with staff warned that adding emojis to social media posts can be enough to count as sharing a personal opinion on an issue. Other news organisations are encouraging journalists to avoid getting sucked into time-consuming arguments on Twitter.

In our survey we find most senior managers (57%) feel that journalists should stick to reporting the news when using social networks like Twitter and Facebook but almost four in ten (38%) feel that they should be able to express their personal opinions openly. To some extent these scores reflect the different traditions in journalism, with public broadcasters concerned that the informal nature of social media communication is undermining trust, while publications with a ‘point of view’ are keen to encourage commentators to express their opinions freely.

The social media presence of journalists is increasingly difficult to navigate. On the one hand, publishers profit from the strong personal brands of some of their correspondents; on the other, many require news staff to be neutral or objective, especially on political and controversial topics. This balance is increasingly hard to achieve in politically and culturally charged settings like social media.

Building on the experience of reporting on COVID, the news industry will turn its attention to the complexities of covering climate change this year. Despite mounting scientific evidence that the world is close to a tipping point from which it may never recover, publishers say it is hard to engage audience interest – and this in turn makes it difficult to make the case for further investment. The World Health Organisation says that climate change is the ‘single biggest health threat facing humanity’27 but only around a third (34%) of publishers think that news coverage is good enough, with a further third (29%) saying it is poor. News organisations have a higher opinion of their own reporting (65%) but this gap suggests that there is more collective work to be done both to raise awareness in general and to make the story relevant to all audiences.

Our survey respondents highlighted six key barriers to better coverage:

What can we expect this year?

Building more scientific expertise in newsrooms: Vincent Giret, Executive News Editor at Radio France, argues that there is a fundamental ‘weakness of scientific culture and background of our newsrooms and our way to select and hire young journalists is too focused on classical and literary backgrounds’. He calls for stronger relationships with academic institutions to help build that understanding. Reuters Global News Editor Jane Barrett also makes the case for expertise: ‘It is too easy for generalist reporters or editors to come to the beat and take every top line as a news story without truly understanding the science and how it fits into the broader picture.’ Others say that the key is to integrate expertise more widely throughout the newsroom: ‘We need to stop being hesitant about calling it the single biggest challenge in the next ten years and to start covering climate change in every single beat – from economy to politics and society’, argues Natalia Viana Rodrigues, Executive Director at the Agência Pública in Brazil.

Constructive and accessible coverage: Others will be trying to move coverage away from a catastrophic narrative. ‘There is plenty of reporting, but most of it is dystopian’, says Götz Hamann, Head of Digital Editions at Die Zeit. The paper has developed a section called Green which tries to find new, more constructive perspectives on climate reporting. For example, it only features interviews about the difference companies are making today, rather than what they might do in the future. Francisco Balsemão, CEO of Portuguese publisher Impresa, argues that ‘Journalists need not only to know their facts but to wrap them up in a way that they are appealing’. Expect to see more effort this year in information graphics and interactive features to engage and involve audiences.

Joint initiatives to tackle climate change: To address the shortage of budget for original climate reporting, survey respondents highlight the benefits of working together. European Perspective facilitates the sharing of original content between participating public broadcasters. Automated translation using AI/machine learning tools is making it easier to make use of this shared content. In the first six months of operation stories generated this way, mostly about climate change, COVID-19, and other science subjects, received 14.5 million page views in eight different languages.

Other examples include the Oxford Climate Journalism Network (OCJN), a new programme of collaboration and scholarship from the Reuters Institute28 and the Rainforest Investigations Network funded by the Pulitzer Center, which is using publicly available data to map forest loss and turn these into stories. It is developing new journalistic skills that mix statistical modelling, data, and cartography.

Impartiality and climate change: One burning issue for journalists in 2022 will be the extent to which news organisations should actively campaign for greener solutions or just report on them. Much of this debate will push into the language used by news organisations and journalists to discuss the subject. The Guardian now uses terms like ‘climate emergency’, ‘climate breakdown’, and ‘global heating’ to convey greater urgency. Expect more debate on these issues in newsrooms this year as pressure grows from younger journalists who believe their organisations should take a more activist stance.

For the last few years, we have tracked the inevitable march towards greater regulation of giant tech companies as they exert a bigger influence over our lives. Much of the debate around regulation has been driven by the lobbying of vested interests (including the platforms themselves and many traditional media companies), but the argument that ‘something should be done’ now appears to be won and we are moving rapidly towards implementation on multiple fronts, including anti-trust, privacy, safety, and more. Having said that, the impact on consumers is likely to take years to play out, with much potential for unintended consequences.

Even in the United States, the home of many of the biggest tech companies, attitudes have hardened over the past year following the storming of the Capitol and the disruption to US democracy, which has at least partly been attributed to social media. Revelations in the so-called Facebook Papers, a treasure trove of internal documents leaked by former product manager Frances Haugen, heaped further pressure on Facebook, now renamed Meta, by suggesting, amongst other things, that executives had put profits before efforts to stamp out hate speech and misinformation. But it’s not just Facebook itself – false information about vaccines spread through YouTube, Instagram, WhatsApp, and TikTok amongst others has undermined public health campaigns across the world, all increasing demands for action.

But news media are only part of governments’ interest in platform power. COVID has dramatically accelerated digitisation of other aspects of the economy and culture such as shopping, film, and other forms of entertainment. And waiting in the wings for regulators are new challenges around cybercrime and artificial intelligence.

What can we expect this year?

Europe leads the way on competition and online harms regulation this year: The EU’s Digital Markets Act (DMA), which looks to curb anti-competitive behaviour amongst the biggest players, and the Digital Services Act (DSA), which aims to regulate online content for a much wider set of intermediaries, are both set to become law this year. At the same time the UK government is planning to pass its much-delayed Online Safety Bill which, amongst other measures, gives new powers to sanction web platforms who fail to curb illegal (and other harmful) content, with compliance regulated by the media watchdog Ofcom. The problem of defining harmful – but not illegal – content hasn’t gone away and will remain the hardest problem to solve in democracies that also value free speech and diverse expression.

More copyright payments for news: For some time, publishers have been looking to extract money from platforms that use or link to their content. Intense lobbying led to the Copyright Directive in Europe and the News Bargaining Code in Australia, as a result of which some big news organisations in France and Australia have received significant sums for licensing content. This year, publishers in countries like Italy and Spain are looking to cash in as national interpretations of the EU Directive come into play.

But critics argue these opaque deals may not be a great model in that they risk entrenching currently dominant platforms and tend to benefit big incumbent players rather than the smaller or local publications that are in most need of support. Expect to hear more sniping from those who feel these deals give an unfair advantage to large legacy publishers with political clout.

Meanwhile the platforms, who launched their own schemes such as Facebook News and Google News Showcase partly as a way of heading off legislation, may review the value of these separate features if they continue to provide little extra value to users.

Government subsidies for local media may get real: With mounting concern about news deserts in the US, there has been growing bipartisan support for measures that could deliver $1.7bn of public subsidy over the next five years. This provision is part of the Build Back Better bill that passed the House of Representatives in November 2021 and would offer a payroll tax credit of up to 50% for journalists employed by local newspapers, digital-only sites, or broadcast outlets.29 Progress is not guaranteed after the bill ran into trouble in the Senate, but if it does eventually succeed it would mark a major change in the US tradition that journalism should remain financially independent of government, and potentially provide a model for other countries too.

Nevertheless, the unstable nature of many government coalitions and their often-fractious relations with journalists means that helpful policy interventions are unlikely to be a priority in many countries this year. The potential is clear: there are a number of existing arrangements in place in some countries that demonstrably work and could be adopted elsewhere, as shown for example in the report A New Deal for Journalism.30 The risk is clear too: that subsidies are tilted towards influential incumbents engaged in rent-seeking, and leave publishers more intertwined with the politicians who control the purse strings.

In our survey we do see our digital leaders becoming more optimistic about the potential impact of legislation and other interventions over the last few years. Four in ten (41%) think policy changes could help journalism, compared with just 18% in 2020. Around a quarter (24%) are worried that interventions could make things worse.

This change in sentiment could reflect a hope that governments are finally prepared to help get a better deal for publishers and clamp down on unreliable and harmful information, but it may also be recognition for practical help received – such as the extension of tax relief on digital subscriptions in many countries.

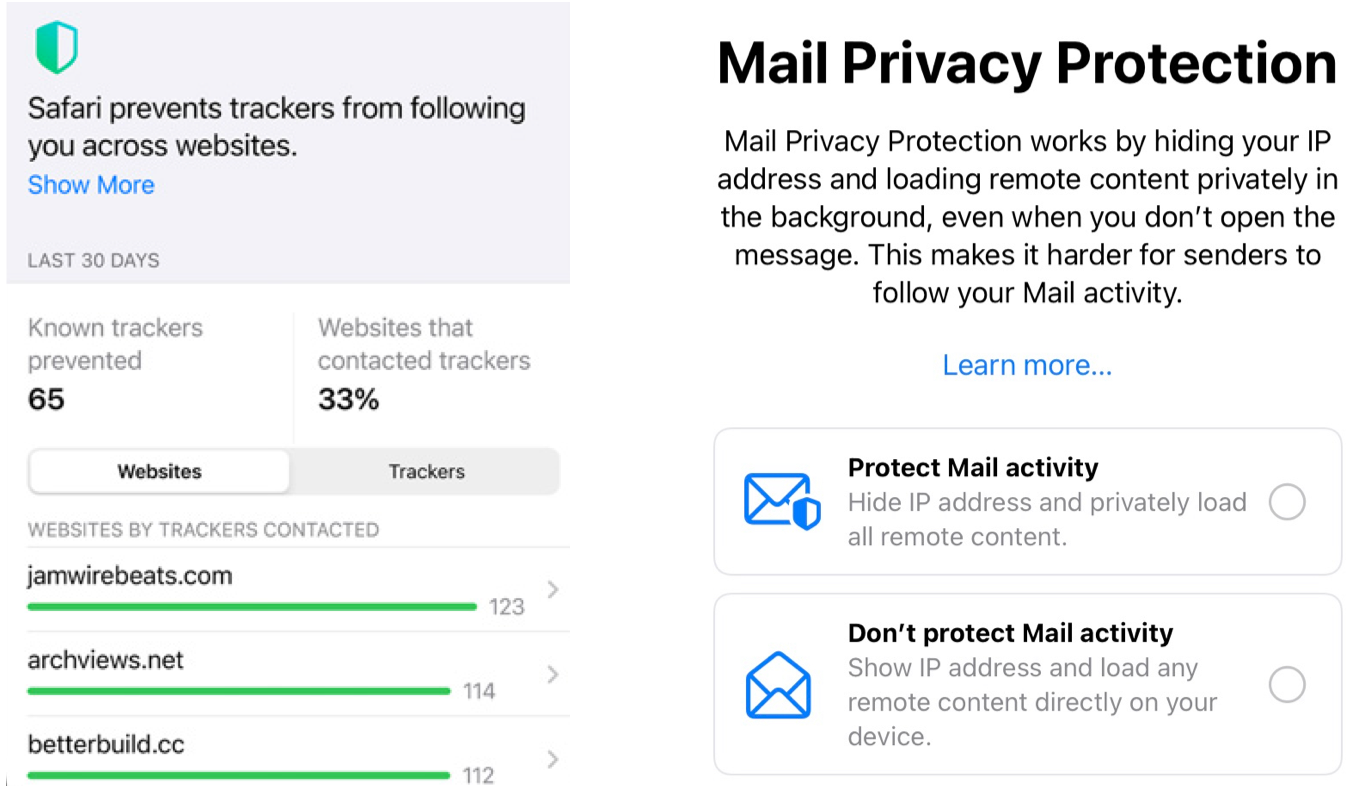

Privacy changes come back to bite publishers: Three years ago, the introduction of the General Data Protection Regulation (GDPR) created a new standard for privacy and data protection. The law has increased data protection awareness and led to significant changes all over the world but many of these have made it harder to track users, offer personalised services, and make money from advertising. GDPR has also done little to reduce consumer confusion, adding a multitude of pop-up messages and interrupting users’ journey to content.

Meanwhile browser and operating-level changes are gradually killing the lucrative practice of firing third-party cookies and other ways to track users across different websites and apps. As one example the release of Apple’s iOS15 stops publishers knowing whether an email has been opened. Given that Apple drives much of the email traffic to publishers, this will make it harder to understand the effectiveness of this critical channel. Google, which owns the most popular web-browser Chrome, has also pledged to stop support for third-party cookies soon and stop other mechanisms like fingerprinting and cache checking.31

As a result, publishers will focus on building first-party data through interactive features, events, and competitions this year. Email publishers in particular will look to build feedback loops into their products to help make the internal case for value.

Looking to the future, start-ups like Bubblr are offering privacy-first, decentralised alternatives to the big platforms that promise to give consumers more control over the advertising they see.32

While most publishers are focusing on making the best of the web that exists today, there will be much excitement – and some hype – about what comes next. Terms like artificial intelligence, Web3, crypto, NFTs, and the metaverse will be heard more and more in the year ahead, but what relevance do they have for journalism?

Artificial intelligence technologies such as Machine Learning (ML), Deep Learning (DL), Natural Language Processing (NLP), and Natural Language Generation (NLG) have become more embedded in every aspect of publishers’ businesses over the last few years. Indeed, these can no longer be regarded as ‘next generation’ technologies but are fast becoming a core part of a modern news operation at every level – from newsgathering and production right through to distribution.

More than eight in ten (85%) say that AI will be very or somewhat important this year in delivering better personalisation and content recommendations for consumers. A similar proportion (81%) see AI as important for automating and speeding up newsroom workflows, such as the tagging of content, assisted subbing, and interview transcription. Others see AI as playing a key part in helping find or investigate stories using data (70%) or helping with commercial strategies (69%), for example in identifying and targeting prospective customers most likely to pay for a subscription. Using AI to automatically write (40%) stories – so-called robo-journalism – is less of a priority at this stage but is where many of the most future-focused publishers are spending their time.

AI gets increasingly fluent

Every year sees more spectacular progress in the world of Natural Language Processing and Generation. In 2020 OpenAI came up with its GPT-3 model, which learns from existing text and can automatically provide different ways of finishing a sentence (think predictive text but for long-form articles). Now Deep Mind, which is owned by Google, has come up with an even larger and more powerful one and these probabilistic models are making an impact in the real world. The ability of AI to write ‘fluent paragraphs’ is now on show at the Wall Street Journal, where it is used to write routine stories about the state of the markets, freeing up journalists to focus on other tasks.33 Meanwhile the BBC is planning to extend its 2019 experiment with election results, which allows hundreds of constituency pages to be automatically written and rewritten by computer as the numbers change – all in a BBC style. Local elections in May 2022 will provide the next test of what will become a permanent system that could be adapted to work with many other types of publicly available data from health to sports and business.

But AI is changing workflows elsewhere

What can we expect in AI this year?

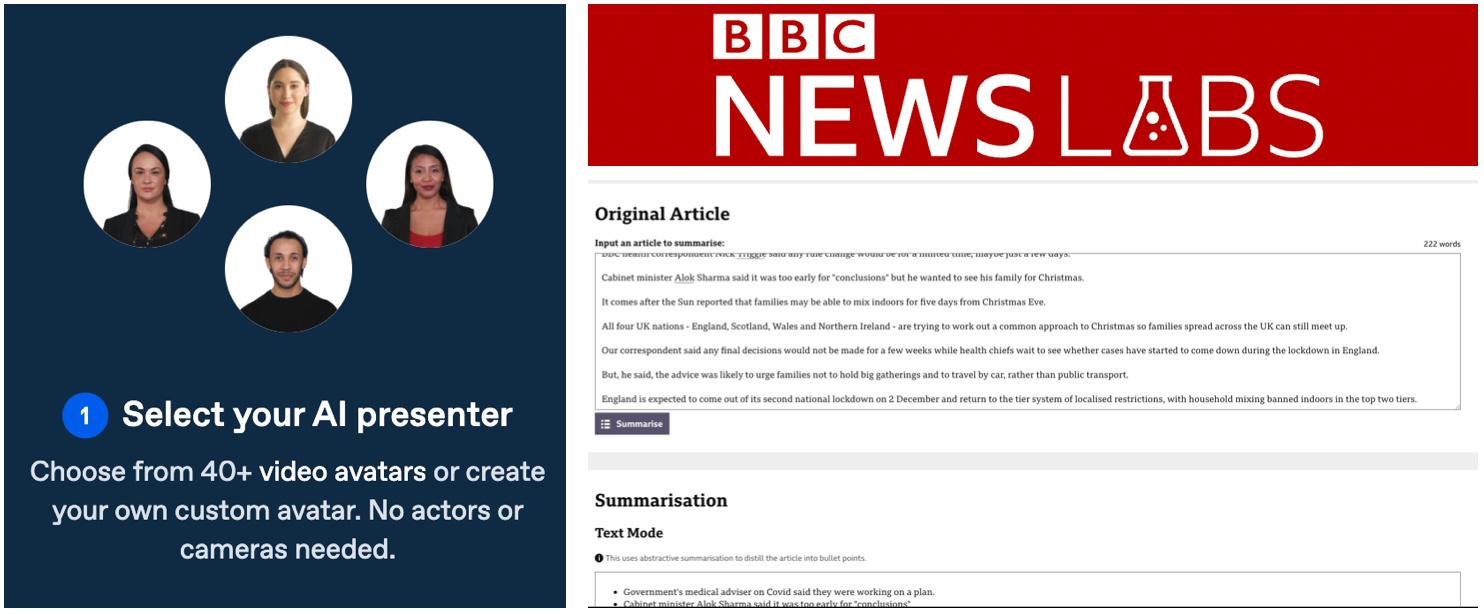

Images and video: the next frontier: DALL-E is a new AI model from Open AI that automates original image creation from instructions you provide in text. This could open up a range of new possibilities, from simple story illustration to entirely new forms of semi-automated visual journalism. In previous predictions reports we’ve highlighted AI systems that can deliver automated or rough-cut videos based on a text story from companies like Wibbitz and Wochit as well as the automated news anchors from companies like Synthesia, which continue to become more lifelike each year.

Why this matters: The big challenge for many large media companies is serving audiences with very different needs using a monolithic website or app. AI offers the possibility of personalising the experience without diluting the integrity of the newsroom agenda by offering different versions of a story – long articles, short articles, summaries, image or video-led treatments – with much greater efficiency.

Summarisation and smart brevity in 2022: Expect to see more experiments with AI-driven formats this year as research shows under-served news audiences prefer:

Digital-born start-ups like Axios have pioneered new editorial forms focused on ‘skim and dig’ behaviours. Automation could go some way to providing similar benefits for general audiences. The BBC’s latest Modus prototype uses two different NLP approaches to generate bullet point-led stories and automated captions for images in picture galleries.

New approach to content management: Enabling this will be a new generation of modular content management systems, such as Arc from the Washington Post and Optimo from the BBC that do not base authoring around a ‘story’ but instead around ‘nested blocks’ that allow better connections across stories, making it easier to reassemble content in potentially limitless ways.

Other AI trends to watch this year

Bridging the AI divide: Up until now the best models for Natural Language Processing and Generation have been focused on English, partly due to the accessibility of data to feed the models. This has been a challenge for less widely spoken languages such as Swedish or even larger ones like Arabic and Spanish where extra training is often needed to get the required quality. But this year expect to see faster progress. Publications like La Nación in Argentina and Inkyfada in Tunisia, which specialises in investigation and data-journalism, have been refining their own models in collaboration with academics.

Productisation eases take-up: Tools such as Trint for automatic transcription, Pinpoint for investigations, and Echobox for identifying the right content to post in social media at the time right time, are also helping to make it easier for smaller newsrooms to get started. Publishers in Scandinavia and elsewhere have developed newsroom tools that identify the gender balance within output to inform editors how well they are representing target audiences. The integration of these tools into content systems will make AI far more accessible and useful this year.

Cooperation and learning: Programmes to share best practice such as the Journalism AI collaboration programme from LSE’s Polis and INMA’s AI webinars and showcases are also helping spread knowledge, enabling small teams to build confidence. The Journalism AI network also enables mentoring for those just starting their AI journeys.35

Improving AI reporting literacy: As with climate change reporting, there is a skills gap around understanding and reporting. AI is throwing up many issues around algorithmic bias, ethics, and regulation, but most journalists don’t have the necessary expertise to hold the big companies to account. One example of what skills might be needed comes from The Markup and its Citizen Browser project, which involved engaging a paid panel of Facebook users prepared to share the content of their news feed.36 This required the publication to analyse huge amounts of data to counter Facebook’s claim that right-wing content, for example, has been getting less popular on the platform.

Facebook changed its name last year to Meta to signal its focus on the metaverse, which Mark Zuckerberg thinks will be the successor to the mobile internet. Others are deeply sceptical, not least because most of the building blocks have still to be put in place and there are so many different visions of what it might be.

The term metaverse was originally coined by Neal Stephenson in his 1992 science fiction novel Snow Crash. Today it broadly describes shared online virtual world environments, many of which already exist in some form (e.g. Second Life, Roblox) but will gradually become more lifelike through the addition of virtual reality (VR) or augmented reality (AR). Others link cryptocurrencies to the concept because in some types of metaverse users buy and trade digital assets based on blockchain technology.

Roblox, for example, has its own virtual currency and has plans to expand from games to other virtual activities such as shopping. Others are focusing on making money from hardware. Meta has a leading position with its Oculus VR headsets, Microsoft has its mixed reality HoloLens and Apple is expected to unveil its VR and mixed reality headset later in 2022, with integration into its existing app ecosystems. AR glasses are set to follow later. With many big companies jostling for position, one big question is whether there will be one metaverse or many. We won’t get the answer to that this year but questions of cross-platform compatibility will become more pressing.

What may happen this year?

Reporting of the metaverse will become more ‘meta’: Expect to see more interviews done in the metaverse itself as the companies themselves try to sell their vision and journalists try, literally, to get their heads round the concept. Journalists have been extremely sceptical so far, partly because of the vagueness of the ideas and partly because the charge is being led by those who created Facebook.

![]()

Workplace may become core use case: Though gaming has been the starting point, it’s likely that mass adoption may also come in the workplace – not least because the pandemic has rapidly shifted the focus from physical to remote interactions.

Just after Facebook rebranded as Meta, Microsoft announced it would be bringing the capabilities of Mesh, its collaborative virtual platform, to Microsoft Teams in 2022. This will enable animated 3D avatars and interactions will work with or without a VR headset. Over time Microsoft says that avatars will start to take on more lifelike facial expressions via signals from webcams. Facebook/Meta is also focusing on the enterprise space, with Horizon Workroom linked to its own Oculus VR headsets. Avatars can interact and draw on whiteboards together, while directional audio will increase the sense of presence.

Sports and news events coverage: Some of the most enthusiastic early adopters have been special events producers in television who are always on the lookout for new techniques to enhance coverage. Broadcasters are adopting mixed reality studios, such as Eurosport’s Cube that allows hosts to see and interact with content around them and to bring celebrities into the studio space from different locations.

All this will make sports (and news) coverage more engaging this year but potentially also confuse the boundaries between what is real and virtually created.

Distribution opportunities for news: It’s still early days but if more time is spent in virtual worlds, at least some of it is bound to be spent with news. Almost 20 years ago the BBC developed a news screen for Second Life and it won’t be long before similar experiences become possible in a range of metaverses near you. Having said that, the challenges of content moderation and oversight that already plague social media could get even worse in spaces powered by VR and AR. An early metaverse demo, for example, was disrupted by a bot spewing misinformation about the dangers of vaccines. Experiences from other nascent virtual worlds also reveal extensive problems with racism, homophobia, and other forms of hate speech.37

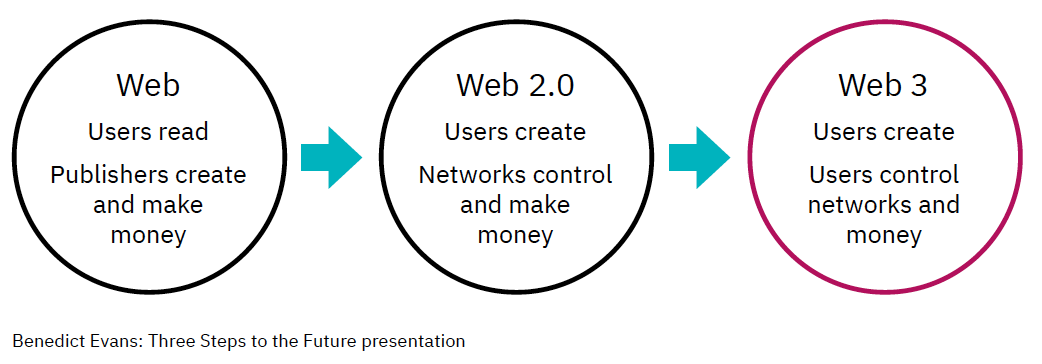

As we’ve already discussed, the development of the metaverse is closely linked with virtual currencies and the idea that digital objects and experiences can be bought and sold in a safe and secure way. This shift is sometimes linked to the next stage of the development of the web which has seen control shift from (1) old gatekeepers to (2) tech platforms and intermediaries and now potentially to (3) individual users and creators themselves. The chart below shows how analyst Benedict Evans describes the possibilities in his annual state of technology presentation.38

Of course, it may not work out this way. It’s hard to see big platforms like Meta building their new systems on a decentralised public blockchain for example and giving away the chance to take their own cut. There is also a problem of trust, with cryptocurrencies still seen in some quarters as little more than a giant Ponzi scheme. At this stage there are still many more questions than answers when it comes to Web3 technologies but we are seeing a few practical examples making waves.

NFTs (non-fungible tokens)

NFT became Collins Dictionary’s Word of the Year for 2021, beating crypto amongst others. The term describes a unique certificate that can record ownership of any digital item such as an artwork, a photograph, or even an original news story. This is lodged in a decentralised public blockchain which serves as record of ownership.

It is this supposedly incorruptible proof has opened the way for the unlocking of enormous value from digital artworks, one of which was sold for $69m in 2021. In another example, the band Kings of Leon generated more than $2.0m when it released its new album as a collection of digital NFTs, with exclusive artwork and limited-edition vinyl. This process is a good example of Web3 principles where the creators are able to bypass traditional gatekeepers in selling directly to the public.

News organisations have been testing the water too. Quartz became the first to sell a news article for a modest $1,800 and the New York Times later raised $860,000 in a similar way – with both organisations donating the money to charity. NFTs are often sold with additional benefits – in the case of the Times this was an audio message from the host of The Daily podcast and the chance to have the winner’s name in the paper.

What may happen this year?

Making NFTs more accessible: This year we can expect to see more uses of NFTs that go beyond art speculation. Publishers could start experimenting with monetising archives that mention family members, or coming up with and auctioning unique membership benefits. That in turn will require a step change in ease of use and ways of accessing the technology. Sports publishers like Turner are building NFTs into e-sports apps, hoping to get a more general audience engaged with trading digital assets and generating loyalty in the process.39 Expect more controversy too over the environmental impact of NFTs which use the same blockchain technology as energy-hungry cryptocurrencies.

This year’s report and survey shows many publishers more determined than ever to refocus their businesses on digital. The ongoing COVID crisis has refashioned behaviours of both consumers and journalists and even when the crisis finally ends, we’ll all be spending more time online and less time together physically. In that context building digital connection and relationships will be more important than ever.

Achieving that will require a laser focus on meeting audience needs, both with content that helps users navigate an increasingly uncertain world but also with products that are more convenient, more relevant, and built around communities of interest. This is why publishers are focusing innovation around their core services as a priority this year, investing in formats like email and audio that are proven to generate loyalty and quality time.

Many publishers are more confident than they have been for some time about the business side, with subscription models paying off and online advertising bouncing back, but with print revenues in inexorable structural decline, and broadcast revenues often stagnant or declining, less digitally advanced parts of the news media may struggle in the years ahead. At the same time there are worrying trends around falling attention for news and politics in some countries – especially at a time of growing extremism and vaccine scepticism.

With a new generation of editors coming through, we will see more focused attempts to engage younger audiences – as well as disaffected ones – with more constructive journalism, as well as by explaining stories better using visuals and data, building on lessons learnt during COVID-19. Improving coverage of complex subjects like climate change and AI will be another theme requiring newsrooms to invest in different kinds of skills and approaches this year.

Understanding the next wave of internet disruption will be critical for the business side too. AI will support the automation of production processes and help to engage audiences in more relevant and personalised ways. The metaverse, Web3, and cryptocurrencies have been largely a subject of novelty or even derision in journalism circles, but a more immersive and distributed web powered by new ways to sell and trade will eventually open up opportunities – as well as challenges – for publishers too. We’ll understand that a bit better by the end of this year.

246 people completed a closed survey in November and December 2021. Participants, drawn from 52 countries, were invited because they held senior positions (editorial, commercial, or product) in traditional or digital-born publishing companies and were responsible for aspects of digital or wider media strategy. The results reflect this strategic sample of select industry leaders, not a representative sample.

2 New York Times Third Quarter Results

6 Twitter - hat tip to Matt Navarra

17 EBU News Report: What’s Next? Public Service Journalism in the Age of Distraction, Opinion and Information Abundance

18 Institute for Strategic Dialogue

25 EBU News Report: What’s Next? Public Service Journalism in the Age of Distraction, Opinion and Information Abundance

26 Center for Media Engagement

Nic Newman is Senior Research Associate at the Reuters Institute for the Study of Journalism, where he has been lead author of the annual Digital News Report since 2012. He is also a consultant on digital media, working actively with news companies on product, audience, and business strategies for digital transition. He has produced a media and journalism predictions report for the last 12 years. This is the sixth to be published by the Reuters Institute.

Nic was a founding member of the BBC News Website, leading international coverage as World Editor (1997–2001). As Head of Product Development (2001–10) he led digital teams, developing websites, mobile, and interactive TV applications for all BBC Journalism sites.

The author is grateful for the input of 246 news leaders from 52 countries/territories, who responded to a survey around the key challenges and opportunities in the year ahead.

Respondents included 57 editors-in-chief, 53 CEOs or managing directors, and 31 heads of digital or innovation and came from some of the world’s leading traditional media companies as well as digital-born organisations (see breakdown at the end of the report).

Survey input and answers helped guide some of the themes in this report and data have been used throughout. Some direct quotes do not carry names or organisations, at the request of those contributors.

The author is particularly grateful to Rasmus Kleis Nielsen for his ideas and suggestions, the research team at the Reuters Institute, and to a range of other experts and media executives who generously contributed their time in background interviews (see fuller list at the end). Thanks also go to Alex Reid for input on the manuscript over the holiday season and keeping the publication on track.

As with many predictions reports there is a significant element of speculation, particularly around specifics and the paper should be read bearing this in mind. Having said that, any mistakes – factual or otherwise – should be considered entirely the responsibility of the author who can be held accountable at the same time next year.

Published by the Reuters Institute for the Study of Journalism with the support of the Google News Initiative.